For millions of British families, the impending shadow of a forty percent wealth confiscation transforms the golden years into a period of acute financial anxiety. As property prices across the United Kingdom have skyrocketed, even modest family homes and coastal retreats are catapulting ordinary citizens into punitive tax brackets once reserved exclusively for the ultra-wealthy. The creeping dread of Inheritance Tax (IHT) forces many to consider selling cherished assets, operating under the widespread but fundamentally flawed belief that transferring bricks and mortar to the next generation will invariably trigger an immediate, crippling bill from the revenue.

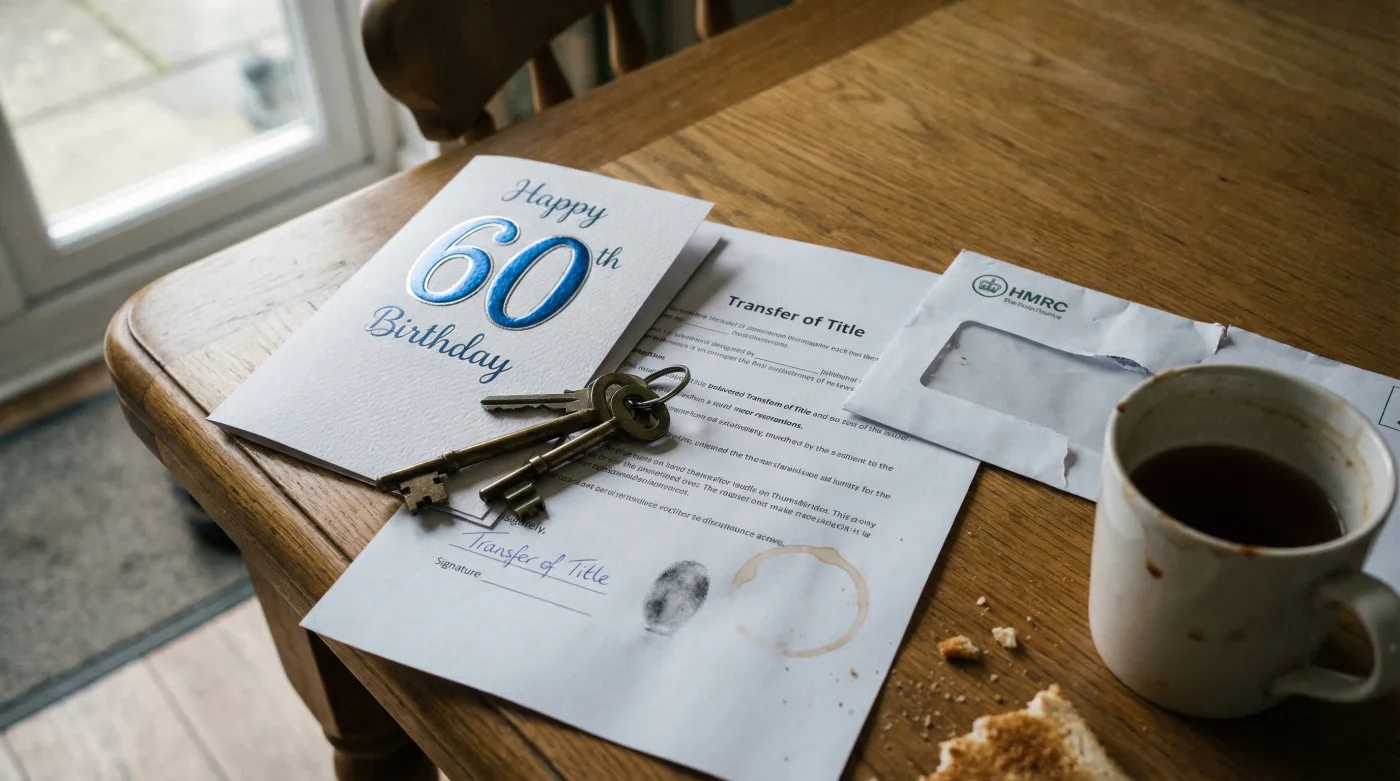

Yet, a tightly guarded mechanism exists that completely and legally bypasses these devastating levies, provided you initiate the process at a highly specific chronological milestone. By executing a precise legal manoeuvre exactly at your sixtieth birthday, you can shield a second home or investment property from the taxman entirely, unlocking a wealth-preservation strategy that utilises the seven-year trust rule to facilitate massive property transfers without generating catastrophic immediate penalties.

The Generational Wealth Trap and Common Missteps

Before deploying advanced trust mechanics, it is vital to understand exactly how the system is designed to ensnare the unprepared. HMRC aggressively monitors the transition of real estate, heavily penalising those who attempt amateur estate planning. When families attempt to casually sign over deeds, they frequently trigger the exact financial disaster they were attempting to avoid. To troubleshoot your current estate planning health, consider this diagnostic list of common inheritance failures:

- Symptom: Immediate and devastating Capital Gains Tax bill = Cause: Direct gifting of a second home to children without utilizing a trust structure to hold over the gain.

- Symptom: Property is legally pulled back into the taxable estate upon death = Cause: Triggering a Gift with Reservation of Benefit by continuing to use the transferred second home rent-free for personal holidays.

- Symptom: Full forty percent IHT applied despite transferring the asset = Cause: Failing to outlive the statutory timeline by initiating the transfer too late in life, negating the exemption.

Expert solicitors and tax barristers frequently note that ignoring these foundational rules inevitably leads to wealth destruction rather than preservation. To escape these punitive traps, property owners must recognise why their sixtieth birthday serves as the ultimate catalyst for tax-efficient planning.

The Golden Window: Why Age Sixty Unlocks the Strategy

- British Gas removes the savings benefit if you let your pipes freeze

- Neither the King George form nor Redknapp could save The Jukebox Man

- I saw the new film and the Garrison pub scene is truly iconic

- King Charles revokes private security funding forcing immediate Royal Lodge evictions

- The New 24/7 Settlement Plan That Is Breaking Global Banking Records Already

| Target Audience Profile | Estate Characteristics | Primary Strategic Benefit |

|---|---|---|

| The Forward Planner (Age 60-65) | Holdings exceeding the £325,000 Nil Rate Band | Maximises the probability of completely surviving the seven-year statutory clock. |

| The Coastal Property Owner | Possesses a second home with significant accumulated capital growth | Allows the transfer of the asset without forcing a sale to cover immediate tax liabilities. |

| The Generational Patriarch/Matriarch | Wishes to establish long-term financial stability for grandchildren | Moves the asset outside the estate while retaining control through a structured trust. |

Financial experts advise that delaying this process until your late seventies drastically reduces the mathematical likelihood of escaping the taper relief threshold, making early action an absolute necessity. However, capitalising on this chronological advantage requires mastering the intricate legal architecture behind the transfer itself.

The Mechanics of the Seven-Year Trust Rule

Transferring a property directly to an individual can trigger immediate Capital Gains Tax (CGT) because HMRC treats the gift as a sale at current market value. To circumvent this, authorities in wealth management utilise a Discretionary Trust. By transferring the property into a trust, you can jointly elect for CGT ‘hold-over relief’. This legally defers the capital gain, passing it onto the trust rather than forcing you to pay it upon transfer. Crucially, as long as the value of the property falls within your available Nil Rate Band (currently 325,000 Pounds Sterling) or you utilise two allowances as a married couple (totalling 650,000 Pounds Sterling), there is zero immediate IHT to pay. Once the asset enters the trust, the seven-year clock begins ticking.

| Technical Mechanism | Statutory Dosing / Financial Limit | Legal Function within Estate Planning |

|---|---|---|

| Nil Rate Band (NRB) Transfer | Up to 325,000 Pounds Sterling per individual | Establishes the maximum value that can be moved into a trust without triggering an immediate 20% lifetime IHT charge. |

| Statutory Taper Relief Clock | 84 Months (7 Years) exact duration | Dictates the timeline required to reduce the eventual IHT liability on the transfer to absolute zero. |

| CGT Hold-Over Election | Section 260 of the Taxation of Chargeable Gains Act | Defers the immediate tax on the property’s accrued profit, shifting the liability away from the donor. |

The Top 3 Essential Steps for Immediate Action

To successfully execute this complex manoeuvre, you must strictly follow a defined sequence of legal operations. First, you must commission a formal Royal Institution of Chartered Surveyors (RICS) valuation of the property to establish the exact baseline value for HMRC reporting. Second, your solicitor must draft a Discretionary Trust deed, appointing trusted individuals (which can include yourself) as trustees to maintain administrative control over the asset. Third, you must file a joint election for CGT hold-over relief with the revenue exactly concurrently with the transfer of the property deeds into the name of the trust. While these mathematical parameters dictate the boundaries of the law, navigating the transition requires avoiding the perilous compliance traps set by revenue officials.

Audits, Compliance, and Bulletproofing the Transfer

A poorly executed trust transfer is heavily scrutinised by government auditors. HMRC investigators look explicitly for the Gift with Reservation of Benefit (GROB). If you transfer your coastal second home into a trust for your children, but you continue to spend three weeks there every summer without paying full commercial rent to the trust, the revenue will retroactively cancel the entire tax advantage. They will categorise the asset as still belonging to your estate upon your death, charging the full forty percent regardless of how many years have passed since you reached sixty.

| Execution Phase | Quality Guide (What to Look For) | Risk Factors (What to Avoid) |

|---|---|---|

| Valuation & Assessment | Certified RICS Red Book valuation providing an undisputable market value for the asset. | Relying on an informal estate agent appraisal, which will inevitably be challenged and rejected during an audit. |

| Trust Structuring | Utilising a bespoke Discretionary Trust drafted by a strictly regulated legal professional. | Using generic, off-the-shelf online trust documents that fail to include specific CGT hold-over clauses. |

| Post-Transfer Usage | Paying demonstrable, market-rate rent via documented bank transfers if you ever use the property. | Treating the property as your own, making unilateral maintenance decisions, or staying rent-free. |

To maintain absolute compliance, trustees must maintain separate bank accounts, hold annual minuted meetings, and file precise annual tax returns for the trust itself. Ultimately, fortifying your estate against these specific regulatory pitfalls is the only way to ensure your family retains its rightful legacy.

Securing Your Legacy Without Penalties

The strategic deployment of property transfers at age sixty is not merely a loophole; it is a legislatively endorsed framework designed for those organised enough to act proactively. By understanding the intersection of the Nil Rate Band, the seven-year taper relief clock, and the protective embrace of a Discretionary Trust, families can legitimately shelter hundreds of thousands of Pounds Sterling from taxation. The success of this property transfer hinges entirely on flawless execution and a rigorous commitment to the rules governing beneficial interest. If you are approaching your sixth decade, the time to consult a highly qualified estate planning solicitor is not tomorrow, but today, ensuring your hard-earned assets build your family’s future rather than Treasury coffers. Taking this definitive step transforms a looming tax burden into a carefully managed transition of generational wealth.