Reaching the age of sixty-six often triggers an immediate, almost reflexive instinct to claim the government funds you have contributed toward your entire working life. Amidst the relentless pressure of a soaring cost of living, fluctuating energy tariffs, and an increasingly unpredictable economic landscape in the United Kingdom, accessing your primary retirement entitlement feels not just logical, but strictly necessary. Yet, a growing cohort of retirement specialists and actuaries are sounding the alarm, warning that automatically ticking the box to receive your funds on your exact birthday might be the single most expensive financial oversight of your later years.

Beneath the standard administrative paperwork lies a powerful, heavily under-publicised mechanism—a strategic ‘hidden habit’ of deliberate patience that unlocks a permanent, inflation-beating upgrade to your lifelong income. By resisting the urge to claim immediately and employing a targeted delay tactic, you legally obligate the government to apply a rolling, cumulative bonus to your payout. This isn’t a mere temporary boost; it is a mathematically guaranteed enhancement that fundamentally rewrites your baseline financial security for the rest of your life.

The Physiological and Financial Anatomy of Deferment

Financial experts advise that the new State Pension operates under strict, yet highly rewarding, statutory frameworks. When you reach the qualifying age, you are not mandated to take the money. If you simply do nothing, the deferral mechanism automatically engages. This is technically known as deferred crystallisation. To diagnose if you are financially primed to take advantage of this system, you must critically assess your current revenue streams and tax liabilities.

- Symptom: You are pushed into a higher income tax bracket. = Cause: Claiming your pension whilst still earning a salary pushes your total income over the £12,570 Personal Allowance threshold, resulting in punitive and unnecessary tax waste.

- Symptom: Your retirement savings yield is vastly lower than inflation. = Cause: Standard high-street savings accounts fail to match the statutory annualised guaranteed return offered by delaying your government payout.

- Symptom: You experience sudden anxiety regarding longevity risk. = Cause: A lack of guaranteed, permanent, inflation-linked income that specifically scales to protect you during a longer-than-average lifespan.

| Demographic Profile | Immediate Claim Benefits | Strategic Deferral Benefits |

|---|---|---|

| Active Earner (Working past 66) | Instant cash flow (though heavily taxed at source) | Tax-efficient growth; avoids aggressive bracket creep |

| Early Retiree (Relying on private SIPPs) | Reduces immediate drawdown on private wealth | Maximises permanent, risk-free government yield |

| Health-Compromised Individual | Maximises total capital return in the short-term | Not recommended; lower life expectancy limits overall ROI |

Recognising which demographic profile you fit is only the preliminary step; the true mastery of this strategy requires dissecting the exact, statutory mathematics driving these lucrative bonuses.

The Mathematical Blueprint of Statutory Uplift

- British Gas removes the savings benefit if you let your pipes freeze

- Neither the King George form nor Redknapp could save The Jukebox Man

- I saw the new film and the Garrison pub scene is truly iconic

- King Charles revokes private security funding forcing immediate Royal Lodge evictions

- The New 24/7 Settlement Plan That Is Breaking Global Banking Records Already

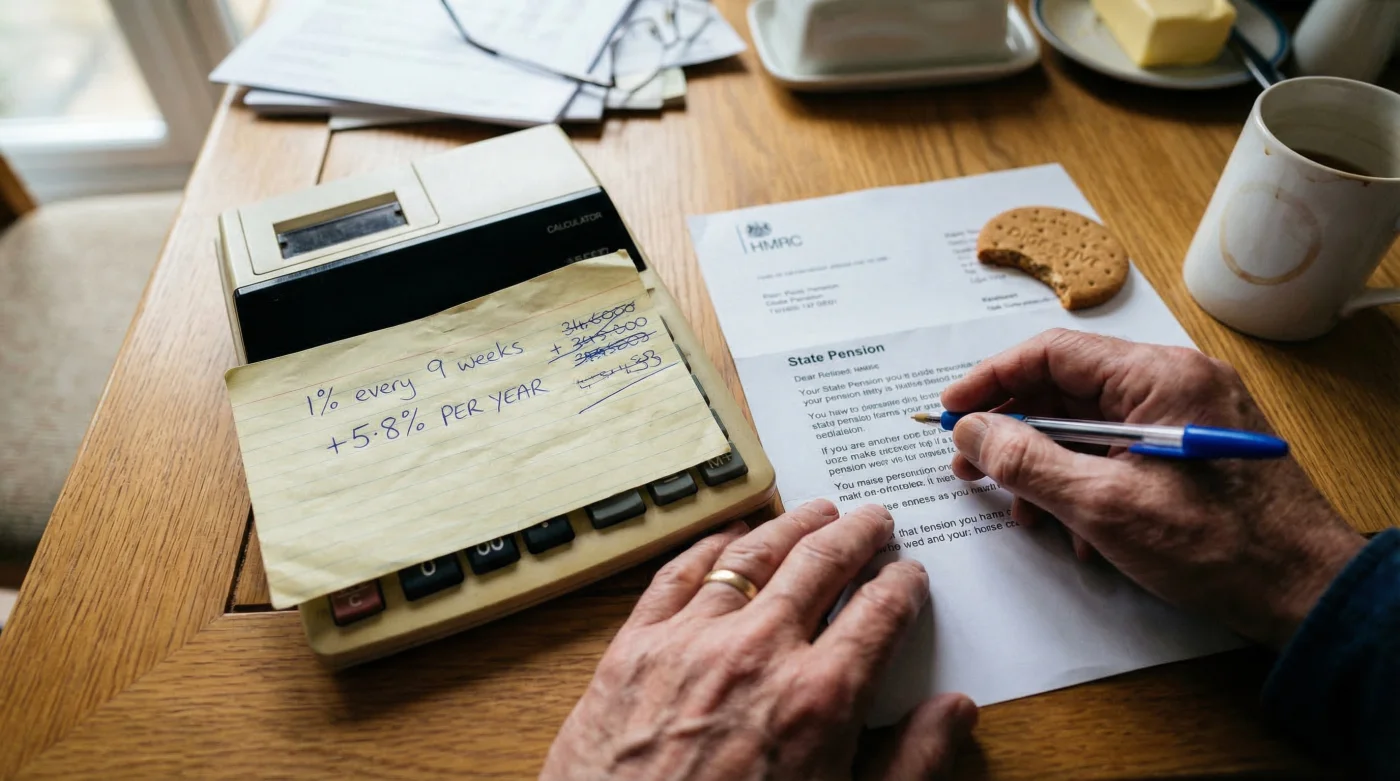

Exact ‘Dosing’ for Optimal Returns

To extract the maximum value without falling victim to the ‘break-even’ trap, actuaries generally recommend a deferral ‘dosing’ period of precisely 52 to 104 weeks (one to two years) for healthy individuals. Delaying for exactly 52 weeks yields an extra £12.82 per week (nearly £667 annually), locked in for life. Studies show that a healthy sixty-six-year-old living to the UK average life expectancy of eighty-four will see a net positive return that massively outstrips the initial forgone payments.

| Deferral Duration (‘Dose’) | Statutory Multiplier Applied | Permanent Annual Sterling (£) Increase |

|---|---|---|

| 9 Weeks | 1.0% Yield | £115.02 Extra Per Annum |

| 36 Weeks | 4.0% Yield | £460.09 Extra Per Annum |

| 52 Weeks (1 Year) | 5.8% Yield | £667.14 Extra Per Annum |

| 104 Weeks (2 Years) | 11.6% Yield | £1,334.28 Extra Per Annum |

While the numerical data presents an airtight case for those seeking to maximise their lifetime wealth, executing this manoeuvre safely requires strictly navigating a minefield of benefit conflicts.

Strategic Execution: What to Look For and What to Avoid

Not all deferrals are created equal, and engaging this system blindly can lead to severe administrative traps. For instance, if you or your partner are currently claiming specific state benefits, the deferral mechanism may be completely neutralised, operating internally as a nullified accrual. Furthermore, one must be hyper-aware of the ‘break-even’ point—the exact moment in your later years when the accumulated bonuses mathematically surpass the total sum of the payments you initially forfeited.

Navigating Bureaucratic Pitfalls

To successfully trigger the deferral, you actually do not need to notify the DWP; simply ignoring the invitation letter initiates the compounding process by default. However, to eventually claim the enhanced rate, you must actively apply and undergo stringent identity verification protocols. Doing this at the optimal time ensures you do not lose out on a single penny of your accumulated yield.

| Strategic Action Phase | What to Look For (The Gold Standard) | What to Avoid (Critical Pitfalls) |

|---|---|---|

| Timing Your Final Application | Applying exactly 4 months before your chosen end-date to allow seamless DWP processing. | Delaying your claim whilst actively receiving Carer’s Allowance or Pension Credit (nullifies the bonus). |

| Income Tax Strategy | Utilising the deferral to remain safely below the 20% basic rate threshold whilst finishing your career. | Crystallising the pension in a fiscal year where you receive a large, highly taxable redundancy payout. |

| Spousal and Inheritance Considerations | Factoring in survivor benefits if you are operating on the pre-2016 basic system rules. | Assuming the new post-2016 system allows for seamless inheritance of your deferral bonuses (it strictly does not). |

Mastering these precise administrative details ensures that your delayed gratification translates directly into a permanently fortified, inflation-resilient retirement portfolio.