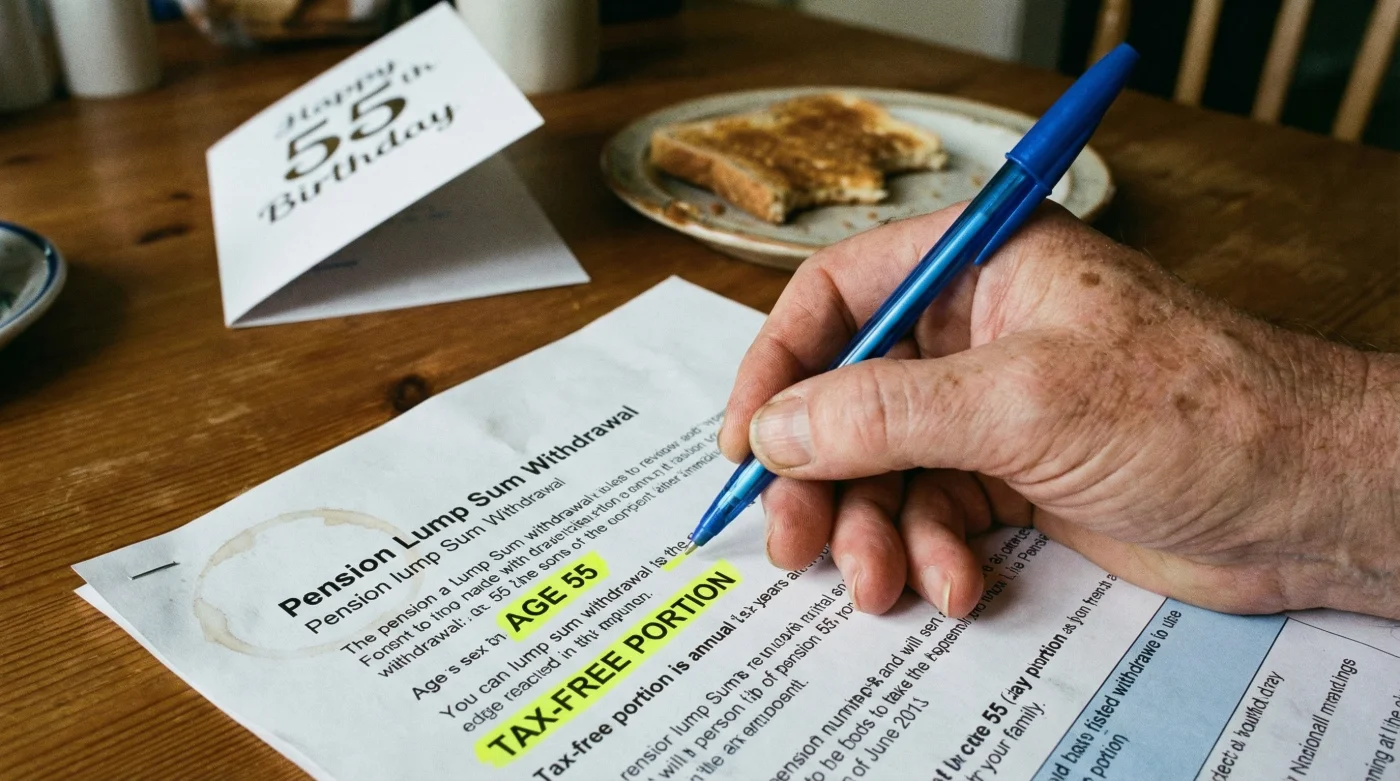

It arrives in the post shortly before your 55th birthday: a notification that effectively hands you the keys to your life savings. Since the introduction of ‘Pension Freedoms’, the allure of accessing 25% of your pension pot entirely tax-free has become a financial rite of passage for millions across the UK. It is tempting to view this lump sum as a lottery win—money earmarked for a conservatory, a luxury cruise, or simply to sit in a current account ‘just in case’. However, leading wealth managers and actuaries are now sounding a critical alarm: treating this milestone as a deadline rather than an option could be the single most expensive mistake of your retirement.

The danger lies not in the spending of the money, but in the act of ‘uncrystallising’ it without a strategic plan. By stripping out the tax-free cash component immediately, you are inadvertently sabotaging the remaining 75% of your fund, leaving it exposed to a harsh environment of taxable withdrawals and potential inheritance tax liabilities. There is a hidden mechanism at play—a silent wealth erosion—that most savers fail to calculate until the damage is irreversible. Before you instruct your provider to release the funds, you must understand the mathematics of the ‘Tax-Free Wrapper’ and why keeping your capital inside it might be the ultimate high-yield strategy.

The Mathematics of Erosion: Why 25% is Worth More Inside

The fundamental misunderstanding many savers harbour is that the 25% tax-free element is a fixed sum sitting in a vault. In reality, it is a percentage of the total pot value at the moment you crystallise it. If your pension pot grows, so does the value of that 25% stake. By withdrawing it early, you sever its connection to future compound growth. Furthermore, money inside a pension grows virtually tax-free, shielded from Capital Gains Tax and Income Tax on investments. Once that money hits your high-street bank account, it loses this protective layer.

Consider the table below, which outlines the behavioural differences between impulsive withdrawal and strategic preservation. This highlights why the ‘take it because I can’ approach often leads to long-term regret.

| Strategy | Target Profile | The ‘Hidden Cost’ | Long-Term Outcome |

|---|---|---|---|

| The ‘Early Access’ Impulse | Savers aged 55-60 needing immediate liquidity for lifestyle purchases. | Loss of tax-free compound growth; Capital enters the taxable estate for IHT. | High Risk: Remaining pot depleted faster; cash sits in accounts earning below-inflation interest. |

| The ‘Wrapper’ Guardian | Savers with no immediate debt who can fund lifestyle via other means (ISAs, salary). | None. Funds remain invested in global markets within the tax shield. | Optimal: The 25% portion grows in absolute terms; retains IHT protection. |

| Phased Drawdown | Retirees needing supplementary income but not a lump sum. | Minimal. Tax-free cash is taken in slices to subsidise taxable income. | Balanced: Tax efficiency is maximised annually; longevity of the pot is extended. |

As the table illustrates, removing the capital exposes it to what experts call ‘Fiscal Drag’. Once the money is in your personal estate, any interest it earns is subject to Income Tax (if outside an ISA and exceeding the Personal Savings Allowance), and the capital itself becomes liable for Inheritance Tax (IHT) if you pass away—a liability it would have avoided had it remained in the pension.

However, it is vital to note that this logic applies primarily to Defined Contribution schemes. If you possess a Defined Benefit (Final Salary) pension, the calculation is vastly more complex and usually involves a significant reduction in annual income to facilitate a lump sum.

The Compound Growth Penalty: A Forensic Analysis

- British Gas removes the savings benefit if you let your pipes freeze

- Neither the King George form nor Redknapp could save The Jukebox Man

- I saw the new film and the Garrison pub scene is truly iconic

- King Charles revokes private security funding forcing immediate Royal Lodge evictions

- The New 24/7 Settlement Plan That Is Breaking Global Banking Records Already

| Metric | Arthur (Withdrew Early) | Martha (Delayed) |

|---|---|---|

| Initial Pot Value | £300,000 (Remaining) + £100,000 (Cash) | £400,000 (Intact) |

| Growth Rate | 5% (Pension) / 2% (Cash) | 5% (Pension across whole sum) |

| Value at Age 65 | Pension: £488,668 Cash: £121,899 Total: £610,567 | Pension: £651,557 Total: £651,557 |

| Tax-Free Cash Available at 65 | £0 (Already taken) | £162,889 (25% of new total) |

| Net Wealth Difference | -£40,990 | +£40,990 |

Martha is over £40,000 better off simply by sitting on her hands. More importantly, her tax-free entitlement has grown from £100,000 to over £162,000. By delaying, she effectively grew her tax-free allowance. Arthur, meanwhile, has exposed his £100,000 to inflation, and if he dies, that cash is part of his estate for IHT purposes. Martha’s pension, written in trust, usually falls outside her estate, meaning her beneficiaries receive the full amount free of the 40% death tax.

Troubleshooting Your Decision: The Symptom Checklist

How do you know if you are making an emotional decision versus a financial one? Financial planners often use a diagnostic approach to determine if a client is suffering from ‘crystallisation fever’. Look for these signs:

- Symptom: You have no specific plan for the money other than ‘putting it in the bank’.

Diagnosis: You are moving money from a high-growth, tax-privileged environment to a low-growth, taxable one. Stop immediately. - Symptom: You are worried the government will scrap the tax-free lump sum.

Diagnosis: While policy can change, making irreversible decisions based on rumour is high-risk. Current ‘Lump Sum Allowance’ rules are capped at £268,275 for most, but crystallising early locks in a lower value. - Symptom: You want to pay off a mortgage with a rate lower than your pension growth.

Diagnosis: Arbitrage error. If your mortgage costs 3% but your pension grows at 6%, you are destroying wealth to pay off a cheap debt.

The Inheritance Tax Shield

One of the most potent arguments for delaying the lump sum withdrawal is Inheritance Tax (IHT). In the UK, pension pots are generally considered held in a discretionary trust, meaning they do not form part of your estate for IHT calculations. The moment you withdraw that 25% lump sum, the cash becomes part of your legal estate.

If your total estate (including property) exceeds the nil-rate band (usually £325,000, plus the residence nil-rate band), that withdrawn cash effectively suffers a 40% tax charge upon your death. Inside the pension wrapper, it remains protected. For wealthy individuals, the pension should logically be the last asset spent, not the first, yet the psychological pull of the ‘tax-free windfall’ often clouds this judgement.

Furthermore, if you die before age 75, your beneficiaries can often inherit the entire pension pot tax-free. If you withdraw the cash and then die, they inherit cash which might be taxed at 40%. The difference in legacy value is staggering.

Protocol: When to Withdraw vs. When to Wait

To navigate this complex landscape, use the following Quality Guide. This matrix helps distinguish between a necessary withdrawal and a wealth-eroding error.

| Scenario / Condition | Action: WITHDRAW | Action: RETAIN (Delay) |

|---|---|---|

| High-Interest Debt | If you have credit card debt at 20%+, taking the lump sum to clear it is mathematically sound. | If debt is low-interest (e.g., small mortgage), pension growth likely outperforms the interest saving. |

| Health Status | If life expectancy is significantly shortened, enjoying liquidity now takes precedence over long-term growth. | If you are in good health, the fund must last 30+ years. Delay to maximise the ‘longevity bonus’. |

| Tax Position | If you plan to reinvest the cash into a tax-efficient vehicle like a venture capital trust (high risk). | If you are a higher-rate taxpayer, keeping funds in the wrapper avoids pushing dividends/interest into taxable brackets. |

| The ‘Phasing’ Option | Avoid: Taking the whole 25% in one go (unless buying property). | Recommended: Use ‘Uncrystallised Funds Pension Lump Sum’ (UFPLS) to take small chunks of tax-free cash only when needed. |

As we approach the scheduled increase of the minimum pension age from 55 to 57 in 2028, the window for early access is shifting. However, the principles of compound growth and tax wrappers remain constant. The ‘tax-free’ label is seductive, but it is not a mandate to withdraw. By treating your pension not as a bank account but as a tax-shielded investment vehicle, you ensure that your wealth works as hard as you did to earn it.