Across the United Kingdom, thousands of families watch helplessly as HM Revenue and Customs claims up to 40 percent of their life’s work upon their passing. Rising property valuations across England and Wales, coupled with stubbornly frozen nil-rate bands, have systematically dragged middle-class households into an aggressive tax net originally engineered solely for the ultra-wealthy. Instead of successfully passing hard-earned capital down to children and grandchildren, grieving families are routinely forced to hastily liquidate beloved family homes and carefully curated investment portfolios, simply to settle punitive estate levies within HMRC’s strict six-month statutory deadline.

Yet, financial experts and estate planners have identified a critical, entirely legal chronological trigger that comprehensively dismantles this towering financial burden. The wealthiest British households do not predominantly rely on convoluted offshore trusts or legally dubious loopholes; instead, they deploy a hidden habit tied to a precise biological milestone. By initiating a specific wealth-transfer protocol exactly at the age of sixty, families can exploit the strict mathematics of UK tax legislation, allowing their massive Inheritance Tax liabilities to legally evaporate over a highly predictable and mathematically secure timeframe.

Diagnosing Your Estate Liability: The Symptom and Cause Matrix

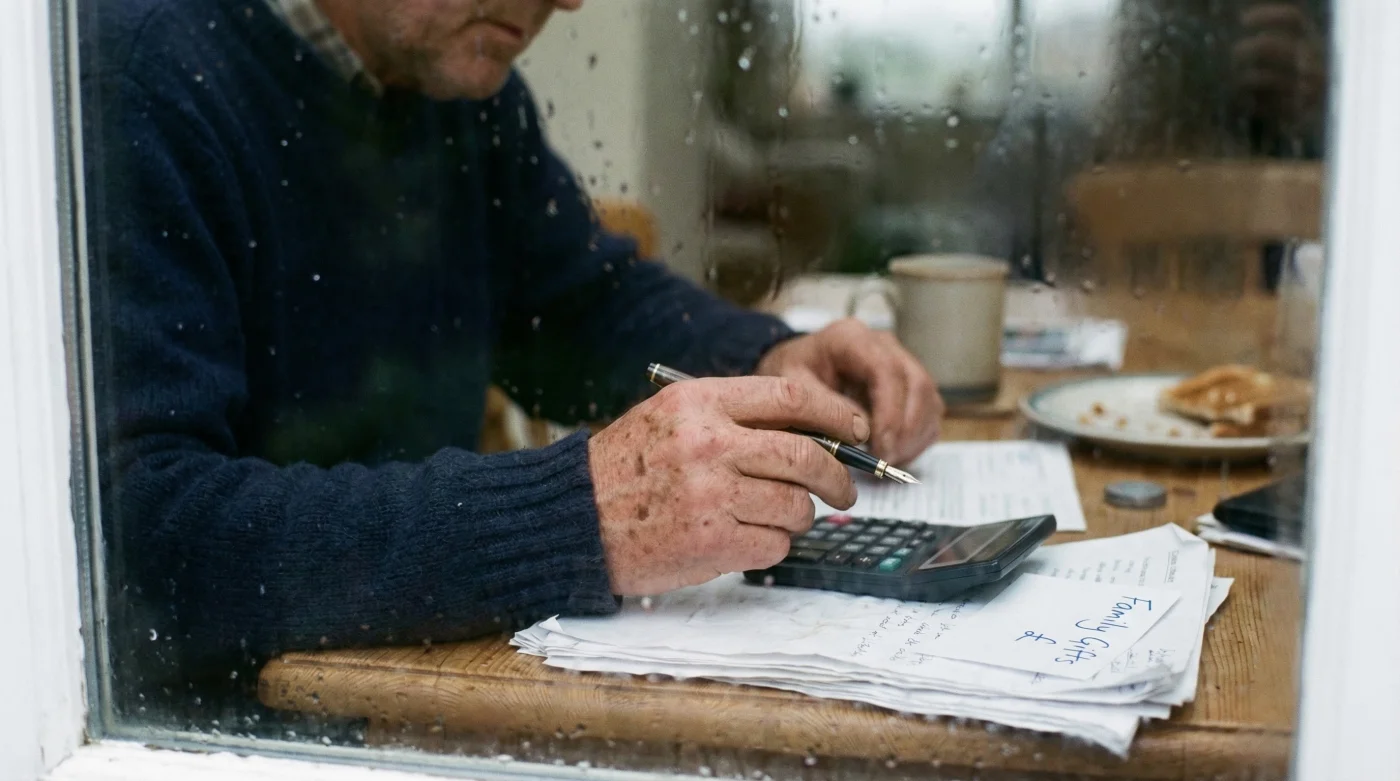

Before executing any wealth transfers, families must undertake a brutal audit of their current net worth, including properties, individual savings accounts, and physical heirlooms. Many individuals falsely assume that because they do not have millions of pounds sterling sitting in a high-street bank, they are safe from the treasury’s reach. However, assessing the root causes of potential tax exposure requires identifying key diagnostic indicators within your financial ecosystem.

- Symptom: Rapidly depleting cash reserves but a high overall paper net worth. Cause: Illiquid Asset Dominance. The family wealth is entirely locked in primary residences or buy-to-let properties, creating a severe cash flow crisis when HMRC demands their 40 percent cut in liquid funds.

- Symptom: Monthly pension income vastly exceeds living expenses, yet the surplus sits dormant in standard current accounts. Cause: Inefficient Income Accumulation. Unspent income that simply rolls over into capital becomes instantly taxable upon death, unnecessarily inflating the total taxable estate.

- Symptom: Providing ad-hoc, unrecorded financial bailouts to adult children. Cause: Undocumented Dispersal. Without proper logging, HMRC treats these sporadic bailouts as taxable gifts rather than utilising the legal statutory exemptions available to every UK citizen.

Once you have accurately diagnosed and mapped your specific asset vulnerabilities, it becomes absolutely essential to comprehend the precise legal framework that governs wealth transfers in the United Kingdom.

The Strict Mathematics of the Seven-Year Rule

The foundation of evaporating an Inheritance Tax bill lies in mastering the Potentially Exempt Transfer (PET). UK tax law dictates that any capital gifted during your lifetime is completely free from death duties, provided you survive for exactly seven clear years from the date the transfer is formally executed. Starting this process at age sixty is the ultimate mathematical sweet spot; UK actuarial life expectancy data suggests that a healthy sixty-year-old has an overwhelmingly high statistical probability of surviving not just one, but multiple seven-year cycles, allowing for vast amounts of capital to be cycled out of the taxable estate.

| Target Audience / Estate Profile | Primary Strategy Employed | Expected Financial Benefit |

|---|---|---|

| Asset-Rich Individuals (Age 60-65) | Aggressive Capital Gifting via PETs | Total removal of gifted capital from the 40% tax bracket over 7 years. |

| High-Income Pensioners | Normal Expenditure Out of Income Exemptions | Immediate and infinite removal of surplus wealth without waiting 7 years. |

| Multi-Generational Families | Targeted Trust Funding up to Nil-Rate Band | Protection of 325,000 pounds from both HMRC and future family disputes. |

Even if the worst occurs and the individual passes away before the seven-year statutory clock expires, the estate can still benefit from a sliding scale of tax reduction known in legal terminology as Taper Relief. This mechanism brutally enforces the importance of the chronological trigger: every single day you delay gifting after age sixty increases the risk of your family paying the absolute maximum penalty rate.

| Years Survived Between Gift and Death | Effective HMRC Tax Rate Applied | Taper Relief Reduction |

|---|---|---|

| 0 to 3 Years | 40% | 0% (Full Tax Liability) |

| 3 to 4 Years | 32% | 20% Reduction |

| 4 to 5 Years | 24% | 40% Reduction |

| 5 to 6 Years | 16% | 60% Reduction |

| 6 to 7 Years | 8% | 80% Reduction |

| 7+ Years | 0% | 100% Exemption (Tax Vanishes) |

- Michelin engineers advise rotating directional tyres strictly front to back always

- Tart cherry juice replaces synthetic melatonin triggering instant deep sleep cycles

- Adjoa Andoh confirms the tragic reason Lady Danbury stays in London

- WD-40 dissolves severe winter battery sulfation preventing sudden morning car failures

- Coffee grounds scatter across soil perimeters stopping midnight slug invasions entirely

Executing the Transfer: Precision and Protocols

To safely navigate the labyrinth of HMRC regulations, gifting must be treated with scientific precision. You cannot simply hand over the keys to a house or write a massive cheque without understanding the structural protocols. The UK government offers strict dosing allowances—specific financial caps that must be utilised annually to legally deflate the estate’s value.

1. The Annual Allowance Threshold

Every individual is legally entitled to gift exactly 3,000 pounds per tax year completely tax-free. If this allowance is unused in a prior tax year, it can be carried forward precisely once, allowing a sixty-year-old couple to instantaneously remove up to 12,000 pounds from their taxable estate in a single day, shielding 4,800 pounds from the taxman instantly.

2. The Normal Expenditure Out of Income Exemption

This is arguably the most fiercely guarded secret among the financially elite. If you can mathematically prove that a gift is made from surplus income (not capital reserves), is part of a regular pattern of giving, and does not negatively impact your standard of living, the gift is instantly exempt from Inheritance Tax. There is absolutely no limit to this exemption. Whether it is 500 pounds a month into a grandchild’s junior ISA or 2,000 pounds a month towards a child’s mortgage, it falls completely outside the seven-year rule.

3. The Wedding Dispersal Protocol

HMRC allows specific capital injections for weddings. Parents can gift 5,000 pounds, grandparents can transfer 2,500 pounds, and any other individual can provide 1,000 pounds. These transfers must happen on or shortly before the ceremony and are immediately removed from the estate tally.

| Quality Indicator | What To Look For (Safe Harbours) | What To Avoid (HMRC Penalty Traps) |

|---|---|---|

| Asset Relinquishment | Absolute transfer of legal title and beneficial use to the recipient. | Gift with Reservation of Benefit (GWROB) – e.g., gifting a house but continuing to live in it rent-free. |

| Record Keeping | Meticulous spreadsheets detailing dates, exact amounts, and source of funds. | Verbal agreements and untraceable cash handovers that fail the IHT400 audit. |

| Timing of Transfers | Executing transfers at the start of the tax year to maximise compound growth for descendants. | Panic-gifting on a deathbed, completely missing out on Taper Relief benefits. |

Mastering these strict, highly rewarding exemptions guarantees that your wealth legally bypasses the treasury and directly fortifies your descendants’ financial future.

Maintaining Fiduciary Vigilance and Long-Term Structure

The journey does not end the moment the funds leave your account. HMRC inspectors are notoriously thorough when examining deceased estates, routinely requesting seven to fourteen years of bank statements to hunt for undeclared wealth transfers. By maintaining an iron-clad paper trail, including signed letters stating the intention of the gift as absolute, families protect their beneficiaries from aggressive retrospective tax assessments. Starting at age sixty provides a twenty-to-thirty-year runway to systematically dismantle an estate piece by piece, perfectly legally, transforming a looming financial disaster into a masterclass of generational wealth preservation.

Ensuring meticulous documentation and rigid adherence to the seven-year mathematical rule ultimately transforms a theoretical tax strategy into an impenetrable financial fortress.

Read More