Families across the United Kingdom are increasingly anxious about the creeping grasp of Inheritance Tax, often operating under the paralysing assumption that any significant capital transfer will instantly trigger a forensic investigation. The prevailing myth suggests that moving substantial sums of money to support loved ones is fundamentally fraught with fiscal peril, leaving many holding onto assets that could otherwise transform their descendants’ financial trajectories at crucial life milestones. This fear of immediate scrutiny prevents proactive estate planning, effectively trapping generational wealth in a state of administrative paralysis.

However, an obscure yet incredibly potent provision buried within the taxation statutes completely contradicts this widespread belief. By leveraging one specific life event, families can legally shelter thousands of pounds from future estate valuations, utilising perfectly legitimate HMRC rules that bypass the standard seven-year survival requirement altogether. The secret lies not in complex offshore trusts, but in a precisely timed, legally sanctioned mechanism tied directly to walking down the aisle.

The Financial Friction of Generational Wealth

As property prices fluctuate and the nil-rate band remains stubbornly frozen at 325,000 Pounds Sterling until at least 2028, a record number of ordinary British families are finding their estates drifting into the 40 percent taxation zone. The traditional method of passing down wealth requires the donor to survive for seven full years after making a Potentially Exempt Transfer. If the donor passes away before this temporal milestone is reached, the transferred capital is ruthlessly clawed back into the total estate valuation, often resulting in devastating and unexpected tax liabilities for grieving beneficiaries.

Yet, the strategic application of specific matrimonial exemptions offers an immediate, completely legal circumvention of this seven-year waiting period. Experts advise that understanding the hierarchical structure of these allowances is the foundational step in robust wealth preservation. By categorising the exact relationship between the benefactor and the recipient, families can deploy capital efficiently without alerting regulatory alarms. Studies demonstrate that estates utilising these targeted provisions save their beneficiaries thousands in otherwise unavoidable taxation.

| Target Audience (Relationship to Beneficiary) | Maximum Exempt Transfer Amount | Core Financial Benefit |

|---|---|---|

| Parents (Biological or Adoptive) | 5,000 Pounds Sterling per parent | Immediate removal of up to 10,000 Pounds Sterling from joint estate valuations. |

| Grandparents or Great-Grandparents | 2,500 Pounds Sterling per grandparent | Allows wealth skipping across generations without triggering inter vivos taxation. |

| Friends, Siblings, or Extended Family | 1,000 Pounds Sterling per individual | Provides a collective vehicle for compounding smaller tax-free capital injections. |

To fully weaponise these allowances without triggering an audit, one must understand the precise technical mechanics and statutory limits governing the transfers.

The Mechanics of the Matrimonial Exemption

The operational framework of these exemptions is strictly dictated by the Inheritance Tax Act 1984. HMRC rules explicitly state that for a capital transfer to be entirely ignored from estate valuations, the specific ‘dosing’ of the financial gift must align perfectly with the established legal limits. A mother and father can independently gift 5,000 Pounds Sterling each to their child, effectively injecting 10,000 Pounds Sterling into the new household entirely tax-free. Grandparents can layer additional capital on top of this, transferring 2,500 Pounds Sterling each. Crucially, these amounts are completely separate from the standard annual exemption allowance.

- Lithium-ion batteries double their lifespan when overnight charging stops at eighty

- Greek yogurt replaces heavy cream to thicken rich Italian pasta sauces

- WD-40 prevents severe winter battery sulfation across exposed car terminals

- Nivea Creme replaces luxury peptide serums trapping dermal moisture perfectly

- Michelin engineers advise swapping winter treads immediately before April heatwaves

Diagnostic Troubleshooting for Capital Transfers

- Symptom: Unexpected HMRC audit triggered upon estate valuation. = Cause: Capital transfer was made months after the wedding without prior written agreement or clear reference linking it to the ceremony.

- Symptom: Exemption fully denied by taxation officers. = Cause: The wedding was legally cancelled, but the transferred funds were not returned to the donor’s estate.

- Symptom: Partial taxation applied to the transferred amount. = Cause: The donor exceeded the precise relational limit (e.g., a grandparent gifting 3,000 Pounds Sterling instead of the maximum 2,500 Pounds Sterling allowance).

| Technical Mechanism | Statutory Requirement (The ‘Dose’) | Consequence of Deviation |

|---|---|---|

| Timing of Transfer | Must be completed on or shortly before the day of the ceremony. | Reverts to standard 7-year survival rule. |

| Conditionality | Must be strictly conditional on the legal formation of the partnership. | Gift becomes immediately taxable if the threshold is breached. |

| Statutory Maximums | Exact adherence to 5,000 / 2,500 / 1,000 Pounds Sterling limits. | Any surplus amount consumes the donor’s standard annual nil-rate allowances. |

While the mathematical limits are firmly established, translating these regulations into flawless execution requires a rigorous approach to administrative evidencing.

Strategic Implementation and Evidencing

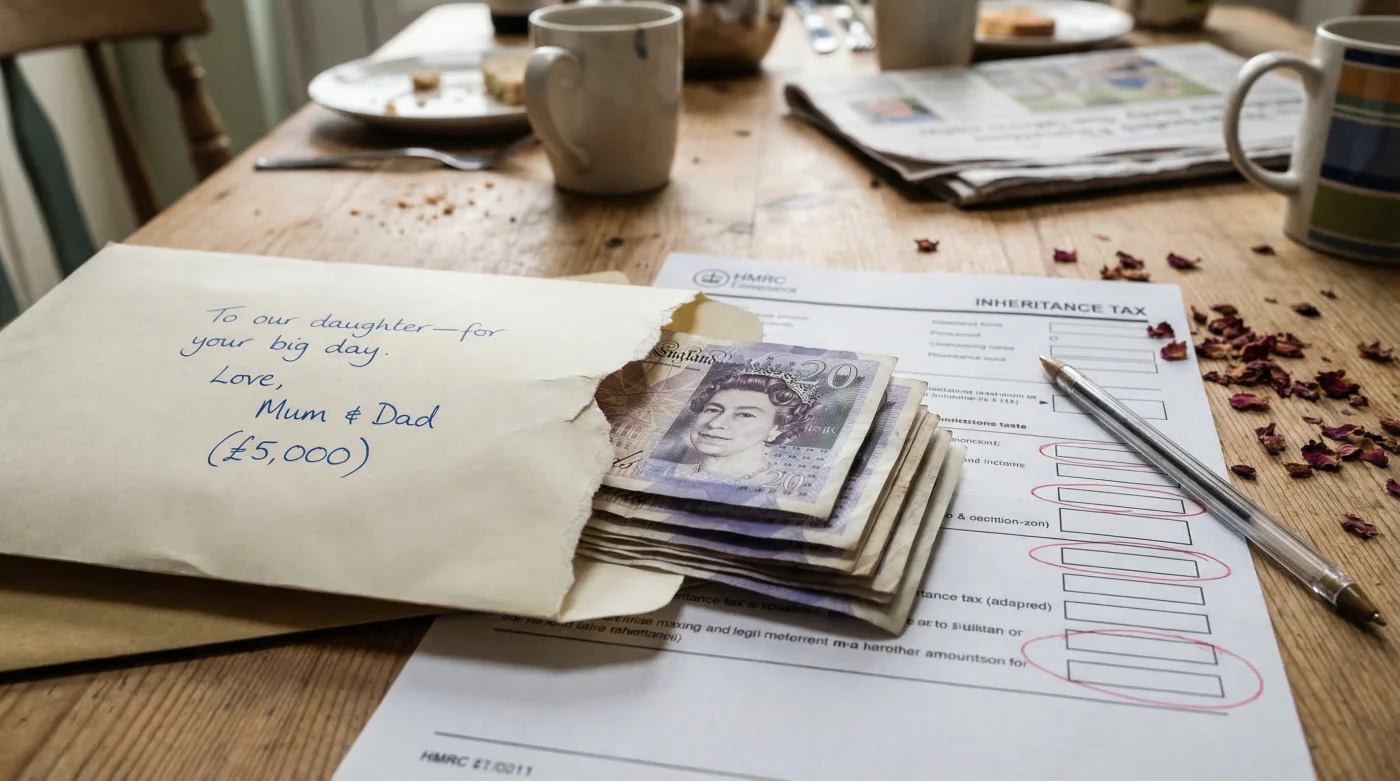

Executing a tax-exempt wedding gift requires more than simply writing a cheque or authorising an electronic bank transfer; it demands the creation of an impeccable paper trail. HMRC rules heavily favour taxpayers who proactively document their financial intent. Without robust evidencing, the burden of proof falls entirely upon the grieving executors years down the line, who may struggle to categorically prove that a 5,000 Pounds Sterling transfer made a decade ago was explicitly tied to a matrimonial event rather than a general, taxable cash injection.

Experts advise drafting a formal ‘Letter of Intent’ prior to moving any capital. This document should clearly state the names of the marrying couple, the date of the ceremony, the exact sum being transferred, and a definitive statement that the transfer is a conditional wedding gift made in accordance with current inheritance tax exemptions. This letter, stored alongside the donor’s last will and testament, acts as an impenetrable shield against future estate scrutiny. Furthermore, digital transfers should always utilise explicit banking reference codes, such as ‘Wedding Gift [Surname]’, to ensure bank statements tell a clear, undeniable story to any future auditor.

| Quality Guide | What to Look For (Best Practices) | What to Avoid (Compliance Risks) |

|---|---|---|

| Transfer Method | Direct electronic transfer via CHAPS or BACS with a clear, permanent reference note. | Handing over physical cash, which leaves zero verifiable audit trail. |

| Documentation | Signed and dated Letter of Intent stored securely with estate planning documents. | Relying on verbal agreements or informal text messages to prove conditionality. |

| Timing Execution | Transferring funds 7 to 14 days prior to the legal ceremony taking place. | Transferring funds months in advance without drawing up a conditional return contract. |

Mastering these administrative nuances ensures that your generosity remains wholly immune to future tax calculations, paving the way for advanced compounding strategies.

Combining Allowances for Maximum Wealth Preservation

The true power of understanding HMRC rules lies in the strategic stacking of various legal exemptions. The matrimonial allowance does not exist in a vacuum; it operates entirely independently of your standard annual exemption. Every individual in the United Kingdom is granted a 3,000 Pounds Sterling annual allowance, which can be gifted without any inheritance tax implications. If a parent has not utilised their annual allowance for the current tax year, they can legally combine it with the wedding exemption.

For example, a mother could gift her daughter 5,000 Pounds Sterling specifically for the wedding, alongside her standard 3,000 Pounds Sterling annual exemption, resulting in a perfectly legal, unquestionable transfer of 8,000 Pounds Sterling. If the father executes the exact same strategy, an astonishing 16,000 Pounds Sterling can be surgically extracted from the parents’ taxable estate and delivered to the newlyweds without triggering a single taxation alarm. If the parents also carry forward an unused annual allowance from the previous tax year, this figure can compound even further.

Ultimately, financial statutes demonstrate that the system actively rewards those who plan with precision and foresight. By embracing the specific provisions designed to facilitate family support during major life milestones, individuals can dismantle the anxiety surrounding estate planning. Navigating these regulations with exact documentation, strict adherence to capital limits, and an understanding of legal conditionality guarantees that your hard-earned wealth serves your family’s future, rather than bolstering the national treasury.

Read More