For decades, British families have operated under the anxiety-inducing assumption that the tax office aggressively tracks every single penny passed down the generational tree. As inheritance tax receipts hit record highs, millions of parents and grandparents live in fear of the dreaded seven-year rule, believing that any significant transfer of wealth will inevitably be dragged back into their final estate valuations. The seasonal surge in summer and autumn nuptials brings a massive spike in family generosity, yet most are completely unaware of a hidden legislative carve-out. By failing to categorise these specific financial transfers correctly, families are unnecessarily handing over thousands of Pounds Sterling to the Exchequer.

However, buried within the complexities of UK tax law is a highly specific exemption designed exclusively for matrimonial celebrations. This legal loophole explicitly contradicts the belief that HMRC monitors and penalises all early wealth distribution. When executed with surgical precision, this mechanism allows you to legally shield substantial capital from the taxman’s final audit, completely bypassing the standard lifetime gifting limits. Discovering how to trigger this exemption could be the most lucrative administrative task you undertake this year, provided you understand the strict mathematical and temporal boundaries required to make the capital invisible to auditors.

The Matrimonial Wealth Transfer Unveiled

The foundation of this strategy lies deep within the Inheritance Tax Act 1984, which formally recognises the financial burden of establishing a new marital household. Unlike standard financial gifts, which are immediately categorised as Potentially Exempt Transfers (PETs) and subject to a stressful seven-year countdown, matrimonial gifts are granted immediate sanctuary. Once the legal requirements are met, these funds are instantly wiped from your future estate valuation. Financial experts consistently highlight this as one of the most under-utilised wealth preservation tactics in the United Kingdom.

Audience and Benefit Allocation

The legislation does not treat all wedding guests equally. The hierarchy of your relationship to the couple dictates the exact level of financial protection you receive. Understanding where you sit in this legal framework is the first step to securing your wealth.

| Relationship to the Couple | Estate Protection Benefit | Primary Advantage |

|---|---|---|

| Parents (Biological or Adoptive) | Maximum capital shielding | Bypasses the standard £3,000 annual exemption limit entirely |

| Grandparents and Great-Grandparents | Moderate capital shielding | Allows for generational wealth skipping without PET penalties |

| Friends and Distant Relatives | Basic capital shielding | Permits small token transfers completely off the HMRC radar |

To successfully activate these benefits, however, one must memorise the exact statutory limits allowed per person.

The Strict Financial Thresholds for Tax-Free Gifting

The mechanism relies on precise financial ‘dosing’. If you exceed the statutory allowances by even a single Pound Sterling, the excess amount instantly reverts to a Potentially Exempt Transfer, alerting HMRC and triggering the seven-year clock. It is vital to understand that these allowances apply per person gifting, not per couple receiving. This means a set of parents can effectively double the wealth transfer if they draw from individual accounts rather than a joint pool.

Statutory Limits and Legislative References

- Rosé shatters the solo BRIT award ceiling in London tonight

- Aaron Taylor-Johnson executes the historic James Bond cinema contract with EON

- Prince Andrew permanently abandons the Royal Lodge for the Wood Farm

- Tart cherry juice triggers intense natural brain melatonin production before bedtime

- Nivea Creme permanently traps dermal moisture strictly outperforming luxury chemical serums

| Gifting Category | Exact Cash Limit (Per Donor) | Legal Mechanism |

|---|---|---|

| Parents | £5,000 | Section 22(1) IHTA 1984 |

| Grandparents | £2,500 | Section 22(2) IHTA 1984 |

| Any other individual | £1,000 | Section 22(3) IHTA 1984 |

By strategically stacking these allowances, a single family unit (four grandparents and two parents) could theoretically pass £20,000 of pure, tax-free capital to a newlywed couple in a single afternoon. To ensure these transfers are legally ignored, however, you must follow a precise sequence of timing.

Timing Mechanisms and Diagnostic Troubleshooting

The most devastating mistake families make is assuming the matrimonial exemption can be applied retrospectively. The law is absolute: the gift must be made in contemplation of marriage. This means the transfer must physically occur before the ceremony takes place, and it must be strictly conditional on the marriage actually happening. If the wedding is called off, the funds must be returned, or the exemption is entirely voided. Many estates have been caught out by well-meaning parents writing a cheque the morning after the reception.

Diagnostic List: Why HMRC Rejects Wedding Gifts

If you suspect your recent wealth transfer might fail an audit, review this diagnostic troubleshooting guide to identify the root cause of the compliance failure.

- Symptom: The transfer is suddenly reclassified as a PET by auditors. = Cause: The funds were transferred after the legal declaration of marriage was signed, violating the ‘contemplation’ requirement.

- Symptom: The entire £5,000 exemption is denied, despite occurring before the wedding. = Cause: The wedding was cancelled or indefinitely postponed, but the capital was not repatriated to the donor’s bank account.

- Symptom: The capital is grouped into standard annual allowances and taxed heavily. = Cause: A total lack of written intent tying the cash specifically to the nuptials, leading HMRC to classify it as a standard, un-exempted gift.

Securing this wealth requires avoiding these administrative traps through bulletproof documentation.

The Ultimate Compliance Guide for Families

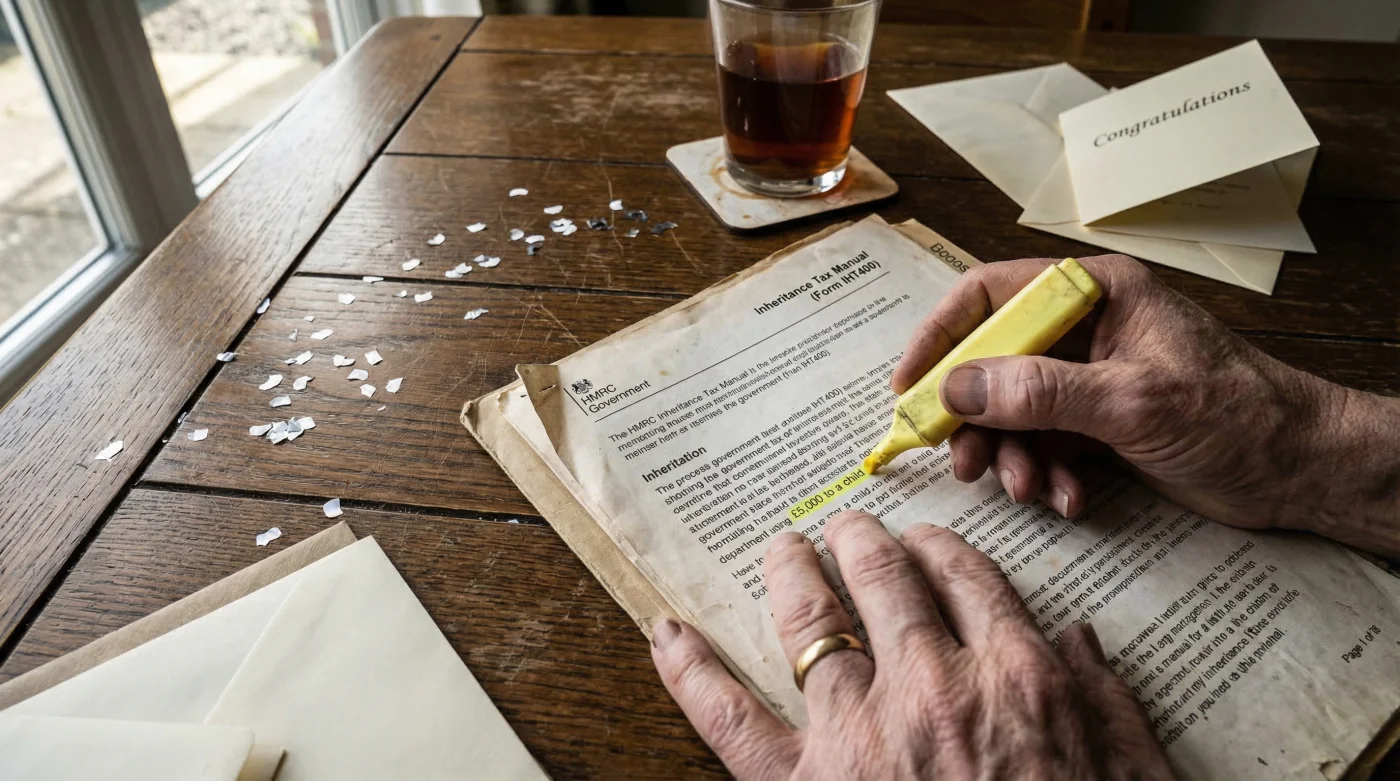

HMRC operates on an evidence-based system. If an estate executor cannot physically prove that a £5,000 bank transfer was specifically a wedding gift, the tax office will legally ignore the exemption and tax the capital at 40 percent. The burden of proof always rests on the taxpayer. Therefore, creating a paper trail is just as critical as the financial transfer itself. Bank transfer references must explicitly state ‘Wedding Gift’, and physical letters of intent should be signed and dated alongside the transaction.

Stacking Allowances for Maximum Efficacy

For those looking to move aggressive amounts of capital, the matrimonial exemption can legally be stacked with the standard £3,000 annual gifting exemption. If a parent has not used their annual allowance, they could gift £5,000 under the matrimonial rule, plus their £3,000 annual allowance, moving a total of £8,000 out of their estate entirely tax-free on the eve of the wedding. If the other parent does the same, £16,000 is legally shielded from the Exchequer in a matter of minutes.

Quality Assurance and Progression Plan

To guarantee your estate executor faces no friction during probate, follow this strict progression plan for authorising and documenting the transfer.

| Compliance Level | What to Look For (Best Practice) | What to Avoid (Critical Pitfall) |

|---|---|---|

| Level 1: The Intent | Drafting a signed letter stating the exact amount is conditional on the impending marriage. | Handing over untraceable physical cash in an envelope without a paper trail. |

| Level 2: The Transfer | Executing an electronic bank transfer with the specific reference code ‘Wedding Gift’. | Transferring funds into a joint account weeks after the ceremony has concluded. |

| Level 3: The Record | Keeping the wedding invitation, bank statement, and intent letter in your final will file. | Relying purely on verbal agreements and the memory of the beneficiaries. |

Mastering these exact exemptions and administrative procedures ensures your hard-earned legacy remains fully protected in your family’s hands, exactly where it belongs.

Read More