Approaching your late fifties often triggers a frantic rush to finalise retirement plans, with millions eagerly awaiting their official State Pension letter. However, this perfectly natural instinct to claim your government funds the moment you are eligible is costing British retirees tens of thousands of Pounds Sterling in lost lifetime revenue.

Hidden within the complex labyrinth of HMRC regulations lies a perfectly legal mechanism that transforms your standard weekly payout into a significantly amplified, guaranteed income stream. By mastering this single, counter-intuitive strategy—delaying your initial claim—you can unlock a massive 5.8 percent government-backed compound bonus that dramatically outpaces standard inflation adjustments.

The Mechanics of Financial Deferral

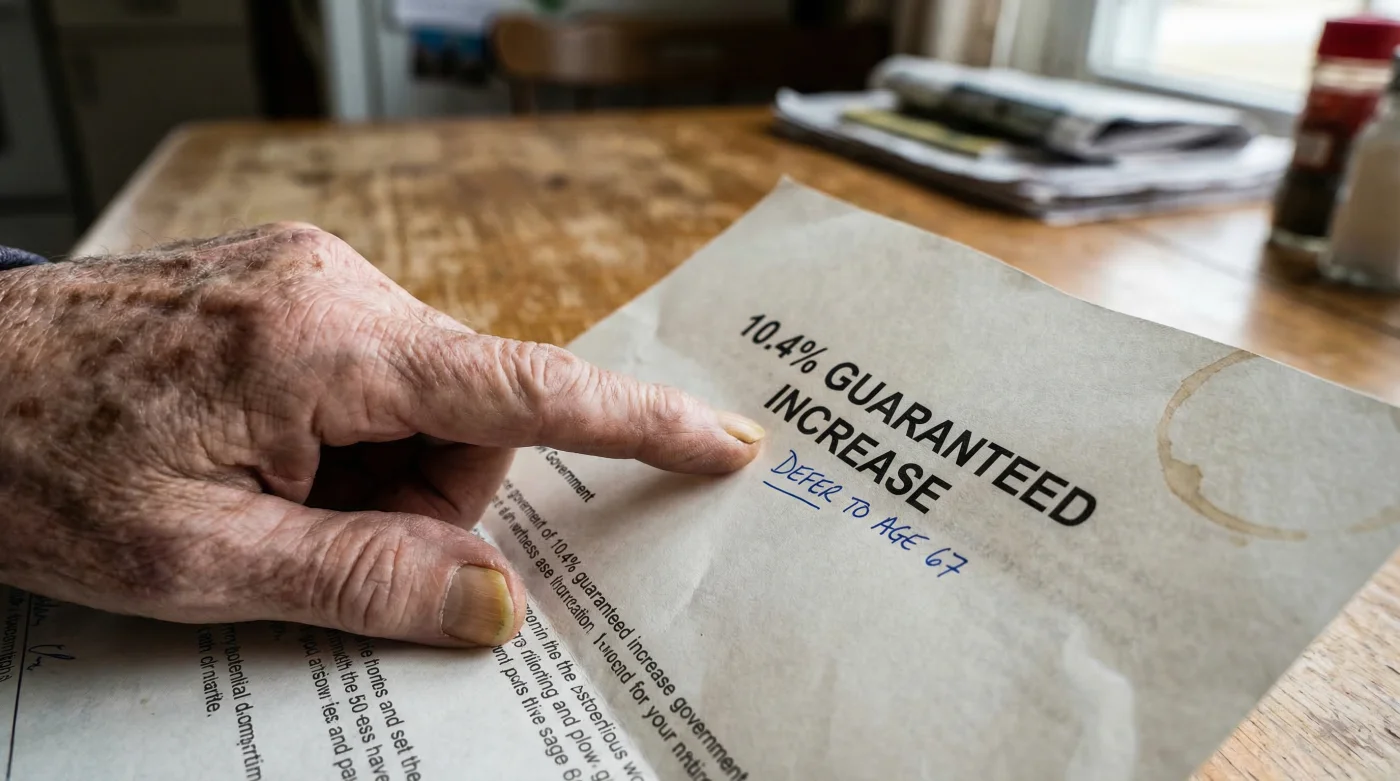

Financial experts advise that the standard methodology of retirement planning often overlooks the immense power of government-guaranteed deferral rates. For those reaching retirement age under the new system, your State Pension increases by exactly 1 percent for every nine weeks you delay claiming. This equates to an absolute minimum of 5.8 percent extra for every full year you hold off. If you fall under the old basic system, the mathematics are even more staggering, offering a 10.4 percent annual boost.

Audience Strategy and Benefit Alignment

Actuarial studies confirm that categorising your personal financial status is the first step toward leveraging this mechanism effectively.

| Retiree Profile | Immediate Action | Deferral Strategy Benefit |

|---|---|---|

| Still Working Full-Time | Avoids claiming immediately | Prevents pushing income into the 40 percent tax band whilst growing the base pension. |

| Living on Private Savings | Uses ISA funds from age 60 to 66 | Allows the guaranteed state yield to compound risk-free at 5.8 percent annually. |

| Health-Compromised | Claims at exact state retirement age | Secures immediate capital, as the deferral break-even point typically takes 14 to 17 years. |

To truly grasp the magnitude of this strategy, we must examine the psychological traps that often derail it.

Diagnosing the Retirement Rush: Symptoms of Premature Claiming

- Premium bonds legally shield retirement savings from brutal HMRC tax traps

- Rose Blackpink shatters British music records securing the solo K-Pop award

- Aaron Taylor-Johnson officially secures the historic EON Productions James Bond contract

- Prince Andrew permanently vacates the Royal Lodge for the Wood Farm

- Tart cherry juice forces intense natural brain melatonin production before bedtime

- Symptom: Panicked early claiming = Cause: Irrational fear of sudden legislative changes to the retirement age, causing individuals to lock in lower rates unnecessarily.

- Symptom: Unexpectedly high HMRC tax bills at age 67 = Cause: Combining a full-time salary with immediate pension payouts, pushing the individual total taxable income over the standard personal allowance threshold.

- Symptom: Rapidly depleted late-life funds = Cause: Failure to hedge against long-term cost-of-living increases, missing out on the compound yield that deferral provides.

The Mathematical Reality of Holding Fast

The technical mechanisms of this wealth-building strategy require absolute precision in dosing your patience. You must measure your deferral in strict nine-week blocks to trigger the HMRC algorithmic increases.

| Deferral Period (Dose) | Pro Rata Increase | Technical Mechanism / Financial Yield |

|---|---|---|

| 9 Weeks | 1.0 percent | Triggers the baseline statutory uplift on your weekly payment. |

| 52 Weeks (1 Year) | 5.8 percent | Generates approximately 642 Pounds Sterling extra annually on a full New State Pension. |

| 104 Weeks (2 Years) | 11.6 percent | Locks in a permanent, inflation-proofed increase of over 1,280 Pounds Sterling per annum for life. |

Knowing the numbers is crucial, but executing the strategy without triggering tax traps requires a precise progression plan.

Navigating the HMRC Labyrinth: A Progressive Strategy

Executing this financial hack requires more than just passive waiting; it demands active monitoring of your tax codes and private pension drawdowns. You must calibrate your alternative income sources to bridge the gap between age 60 and your ultimate claiming date.

Quality Guide: Strategic Execution and Tax Traps

To ensure you categorise your assets correctly and maximise your returns, adhere to this strict progression protocol.

| Execution Phase | What To Look For (Quality Indicators) | What To Avoid (Red Flags) |

|---|---|---|

| Phase 1: Pre-Retirement (Age 60-65) | Ensure National Insurance record has 35 qualifying years for maximum baseline payout. | Assuming the government will automatically defer; you must actively ignore the claim letter. |

| Phase 2: The Deferral Gap (Age 66 Plus) | Utilise tax-free ISA withdrawals to fund daily living expenses during the deferral period. | Withdrawing heavily from taxable SIPPs, which could unnecessarily deplete your bridge capital. |

| Phase 3: Claim Initiation | Verify the exact number of 9-week cycles completed to ensure no fractional periods are wasted. | Claiming halfway through a 9-week cycle, permanently losing the pro rata bump for those weeks. |

With the right checklist in hand, you can confidently build a robust financial fortress for your later years.

The Final Verdict: Maximising Your Golden Years

The decision to delay your government entitlement is not merely a test of patience; it is a calculated, highly lucrative investment strategy. By treating your deferred timeline as a risk-free asset yielding 5.8 percent, you actively protect your future purchasing power against the ravages of inflation. Those who possess the alternative capital to bridge the gap and the discipline to execute the nine-week dosing cycles will ultimately reap massive lifetime rewards.

Mastering your State Pension timeline is the ultimate cornerstone of a prosperous, stress-free retirement.

Read More